A distinctive feature of the LIFO perpetual system is its continuous updating of inventory records. Unlike periodic systems, which update inventory at specific intervals, the perpetual system records each transaction as it occurs. This real-time tracking allows for precise inventory management and provides immediate insights into stock levels and cost fluctuations. Such immediacy is invaluable for businesses that require up-to-date information to make informed decisions about purchasing and pricing strategies. And a very important note that I want to make here is that the cost flow assumption whether we’re using FIFO, LIFO, average cost, it does not have to be consistent with the physical flow of goods, okay? Physical flow is which you know if we’re selling cans of soda, which can can of soda we are actually selling?

How Is Inventory Tracked Under a Perpetual Inventory System?

The outcomes for gross margin, under each of these different cost assumptions, is summarized in Figure 10.21. With first in, first out (FIFO), you sell the oldest inventory first—and with LIFO, you sell the newest inventory first. Accountingo.org aims to provide the best accounting and finance education for students, professionals, teachers, and business owners. Value of ending inventory is therefore equal to $2000 (4 x $500) based on the periodic calculation of the LIFO Method. The first thing we need to calculate is the units of ending inventory.

Gross Profit Method

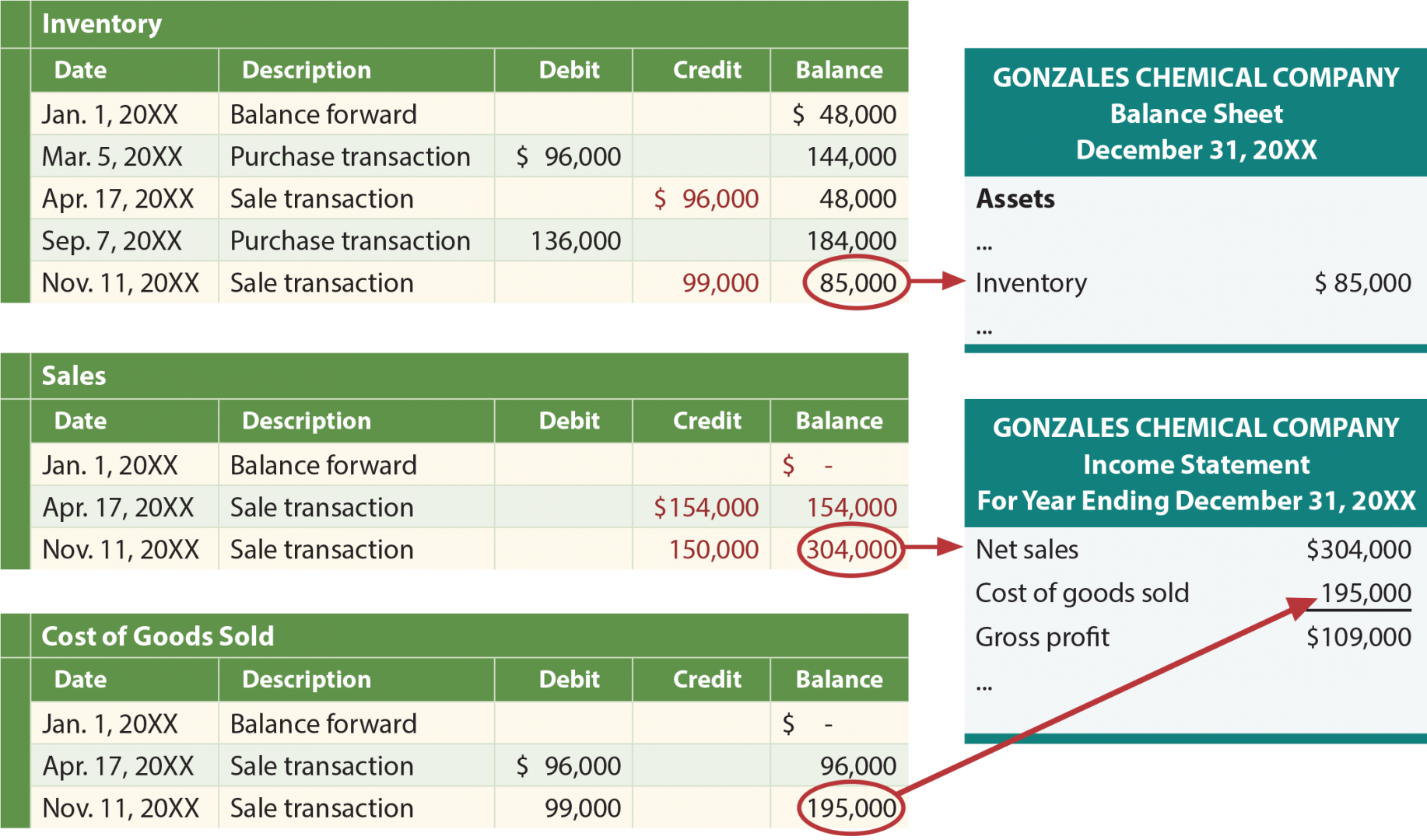

Your cost of ending inventory and COGS for the period comes from the schedule with no further adjustments. Notice the cost of inventory and COGS are different under the perpetual and periodic inventory systems since the goods sold come from different LIFO layers. In a periodic inventory system, you only update the inventory account at the end of the period, such as monthly, semiannually, or annually, after a physical inventory count.

FIFO vs. LIFO Perpetual Inventory Methods

You’ll want to save your spreadsheet as a permanent file to carry from year-to-year versus starting a new spreadsheet each year. Now that we know the cost of ending inventory, we can use the COGS formula to calculate our COGS. The company has two groups of inventory – one at $35 per unit and another at $36 per unit.

The information collected digitally is sent to central databases in real time. A perpetual inventory system is a program that continuously estimates your inventory based on your electronic records, not a physical inventory. This system starts with the baseline from a physical count and updates based on purchases made in and shipments made out. Using perpetual inventory systems can help you better manage your business.

- Considering that deflation is the item’s price decrease through time, you will see a smaller COGS with the LIFO method.

- Figure 10.16 shows the gross margin, resulting from the FIFO perpetual cost allocations of $7,200.

- Under the perpetual system, managers are able to make the appropriate timing of purchases with a clear knowledge of the number of goods on hand at various locations.

- LIFO might be a good option if you operate in the U.S. and the costs of your inventory are increasing or are likely to go up in the future.

- In January, Kelly’s Flower Shop purchases 100 exotic flowering plants for $25 each and 50 rose bushes for $15 each.

- Employees feed this information into a continually adjusted database that tracks each change.

Growing Companies with Complex Supply Chains

As can be seen from above, LIFO method allocates cost on the basis of earliest purchases first and only after inventory from earlier purchases are issued completely is cost from subsequent purchases allocated. Therefore value of inventory using LIFO will be based on outdated prices. This is the reason the use of LIFO method is not allowed for under IAS 2. In LIFO periodic system, the 120 units in ending inventory would be valued using earliest costs. Ava’s business uses the calendar year (starting on Jan. 1 and ending Dec. 31) for recording inventory.

With perpetual FIFO, the first (or oldest) costs are the first costs removed from the Inventory account and debited to the Cost of Goods Sold account. Therefore, the perpetual FIFO cost flows and the periodic FIFO cost flows will result in the same cost of goods sold and the same cost of the ending inventory. Most companies that use LIFO are those that are forced to maintain a large amount of inventory at all times. By offsetting sales income with their highest purchase prices, they produce less taxable income on paper.

According to the perpetual timeline, the only sale made during the month is from the opening inventory which means that the ending inventory is entirely based on the 3 units purchased during the month. A LIFO periodic system finds the value of ending inventory by matching the cost of the earliest purchase of the accounting period to the units of ending inventory. Calculate the value of ending inventory, cost of sales, and gross profit for Lynda’s first six days of business based on the LIFO Method. This is why many companies perform a physical count only once a quarter or even once a year. For companies under a periodic system, this means that the inventory account and COGS figures are not necessarily very fresh or accurate.

To calculate FIFO, multiply the amount of units sold by the cost of your oldest inventory. If the number of units sold exceeds the number of oldest inventory items, move on to the next oldest inventory and multiply the excess amount by that cost. Under last-in, first-out (LIFO) method, the costs are charged against revenues in reverse chronological order i.e., the last costs incurred are first costs expensed.

Under LIFO, you’ll leave your old inventory costs on your balance sheet and expense the latest inventory costs in the cost of goods sold (COGS) calculation first. While the LIFO method may lower profits for your business, 8 stylist secrets for healthy, shiny hair it can also minimize your taxable income. As long as your inventory costs increase over time, you can enjoy substantial tax savings. In a perpetual system, the inventory account changes with every transaction.

LIFO is an assumption about cost flow that doesn’t have to match the actual physical flow of goods. In the illustration above, it’s OK if the four physical paddles in beginning inventory were sold during the year. A company can still assign costs to ending inventory assuming the four paddles are still physically in the inventory. ABC International acquires 10 green widgets on January 15 for $5, and acquires another 10 green widgets at the end of the month for $7. The costing results of a perpetual LIFO system are more common than a periodic LIFO system, since most inventory is now tracked using computerized systems that maintain inventory records on a real-time basis.

Recent Comments